This article was written by Wolf Richter and originally published at Wolf Street

In the world of struggling businesses, debt defaults, bankruptcies, and closures, there is now a clear dividing line.

On one side are those businesses that got bailed out by the government, whether they needed it or not, such as the $25 billion in grants and loans for a handful of airlines, or the $525 billion in PPP loans handed to 5.2 million business entities, from minuscule to large, and some fraudulent. On the same side are businesses with access to the capital markets that got bailed out by the Fed whose corporate bond buying programs drove credit markets into frenzy, eager to fund nearly anything.

But on the other side, are those businesses who didn’t get any of this – neither from the government, nor from the Fed, nor from the frenzied credit markets; and those businesses, often already limping for a while, got run over by the Pandemic.

In terms of publicly traded companies.

In September, another 54 large companies filed for bankruptcy, after 54 had already filed for bankruptcy in August, according to S&P Global Market Intelligence, bringing the total for the year as of October 4 to 509, the highest for the same period since 2010.

These are companies that are either publicly traded (minimum $2 million in assets or liabilities), or are private companies with debt that is publicly traded (minimum $10 million).

The largest bankruptcy filers in September included two Texas-based oil and gas producers: Oasis Petroleum, with over $3 billion in liabilities; and Lonestar Resources with $626 million in liabilities.

Energy companies were only in third place among the sectors with the most bankruptcy filings year-to-date. Here are the S&P’s top five bankruptcy sectors, with the number of filings so far:

- Consumer discretionary: 103

- Industrials: 70

- Energy: 58

- Healthcare 47

- Consumer staples: 27

The long list of chain-store retailers that have filed for bankruptcy during the Pandemic got longer in September with filings, among others, by off-price department store Century 21 (Sep 10), candy-seller It’Surgar (Sep 23), and Forever 21 (Sep 30).

Many retailers, when they file for bankruptcy, end up getting liquidated.

The Federal Reserve Bank of San Francisco, fretting about over-indebted companies becoming even more over-indebted during the Pandemic, said that the number of companies that have defaulted on their debt this year so far “is on course to be the highest since 2009.”

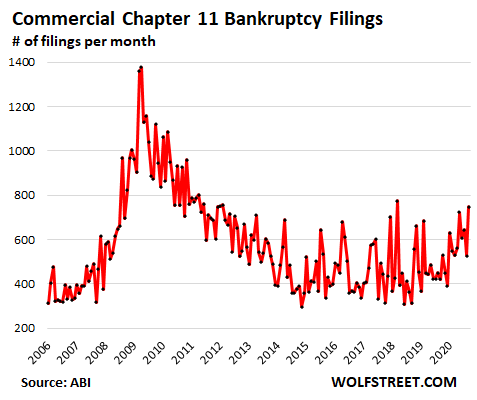

Commercial Chapter 11 bankruptcy filings surge.

This type of filing occurs when a business attempts to restructure its debts while continuing operations, usually with shareholders losing the company, and with creditors taking it. Chapter 11 filings are seasonal, spiking during tax season in March or April. With the tax-filing deadline moved to July 15 this year, the spring spike stretched out over five months. And you would expect, given seasonal patterns, that filings would then taper off. But that’s not what happened.

In September, commercial Chapter 11 filings jumped by 78% year-over-year to 747 filings, the highest since the seasonal spike in March 2018, and beyond that the highest since 2012, according to data released today by the American Bankruptcy Institute. It was the seventh month of double-digit year-over-year increases. From March through September, commercial Chapter 11 filings jumped 40%, compared to the same period last year. Clearly, these companies didn’t get any bailouts:

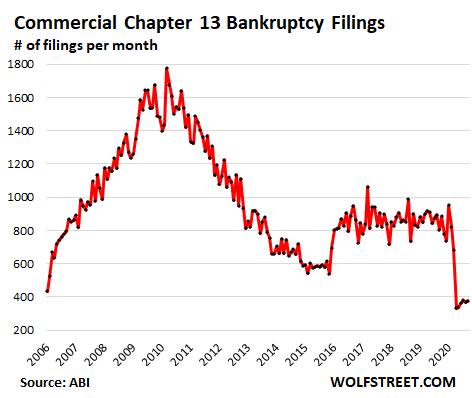

Most small businesses, when they file for bankruptcy, do so either under Chapter 7 (for corporations, partnerships, LLCs, and sole proprietorships) or under Chapter 13 (individuals only, such as sole proprietorships).

Commercial Chapter 13 bankruptcy filings.

The ABI separates out “commercial” Chapter 13 filings from personal Chapter 13 filings. Commercial Chapter 13 filings are filed by individuals whose sole-proprietor business could no longer pay its obligations, such as bank loans, shop rent, goods suppliers, etc.

But here is the thing: The owners of these small businesses were among the recipients of the PPP loans, and among the recipients of the federal unemployment program for the self-employed (PUA) and then the extra $600 a week in unemployment benefits.

A record number of small businesses “quietly” shut down (more on that in a moment), and many of the owners didn’t need to file for bankruptcy because the inflow of government cash allowed them to pay their obligations, work out a deal with the landlord, and shoulder the remaining burden. So commercial Chapter 13 bankruptcy filings plunged in April to just 332, the lowest in the ABI data going back to 2006, and have ticked up only a little since then, with 377 filings in September – an amazing sight during an economic crisis:

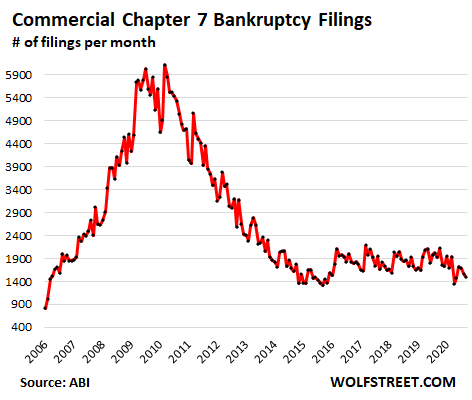

Commercial Chapter 7 filings.

These filings by corporate entities, partnerships, and individuals (sole proprietorships) dropped in April to the lowest since 2015, and have since then zig-zagged higher, but remain low, with 1,503 filings in September. These types of businesses too were among the recipients of the PPP loans, if they continued operations; and most recipients of PPP loans didn’t file for bankruptcy. And many of the individuals who shut down their businesses were among the recipients of PUA benefits and the extra $600 a week and could pay off their creditors and shoulder the rest.

Consumers are still flush with government cash.

Consumer bankruptcy filings fell 36% in September, compared to a year ago, to 37,024 filings, as consumers were still flush with government stimulus money and the extra unemployment benefits of $600 a week through July, and the $300 a week for at least four weeks afterwards, much of which was processed late and arrived in lump-sum payments weeks or months late, therefore dragging into the fall. We have seen this stimulus money play out in record retail sales and record reduction in credit card debt.

Small businesses closed quietly.

From March through mid-July, over 420,00 small businesses – or 7.1% of all small businesses – permanently and quietly closed their doors, more than typically in an entire year, according to a study by Brookings, released in September.

The analysis found that “many small businesses are financially fragile and not equipped to weather a prolonged period of substantially reduced revenues”:

- 47% rely on personal funds of the owner to fill a two-month revenue drop.

- 88% rely on the personal credit score of the owner (such as working capital funded by personal credit cards).

- Only 44% have had a bank loan over the past five years.

Small businesses account for about 99% of all businesses in the US and about 47% of jobs in businesses. If these 420,000 businesses are representative of national employment, “this means we have lost at least 4 million jobs that will only return with the creation of new businesses,” the report said.

Small businesses are prone to failure. But also many new small businesses are being created. This process of new businesses being created has now restarted strongly, but has been far outstripped by the tsunami of business closures. The report:

Even if for the remainder of the year losses simply keep pace with those in previous years, we will see a doubling of the ordinary annual rate of small business losses to more than 700,000 (or 12 percent).That likely optimistic scenario would see around 50 percent more business losses than at the peak of the Great Recession, and the largest loss of small businesses since records began in 1977.

This speaks of the large-scale damage to American businesses. While some businesses massively benefited from the crisis, many more took on heavy damage; and of them, many already shut down, and more will shut down – most of them quietly, and only some with bankruptcy filings.

And without all this stimulus and bailout money?

The biggest programs have ended: the PPP loans for smaller businesses, the Payroll Support Program for larger businesses, the extra $600 a week in unemployment benefits, and the extra $300 a week in unemployment benefits. President Trump, in a series of tweets just now, pulled the rug out from under bailout negotiations until after the election. So for now, it looks like businesses will have to deal with this economy on their own.

With global tensions spiking, thousands of Americans are moving their IRA or 401(k) into an IRA backed by physical gold. Now, thanks to a little-known IRS Tax Law, you can too. Learn how with a free info kit on gold from Birch Gold Group. It reveals how physical precious metals can protect your savings, and how to open a Gold IRA. Click here to get your free Info Kit on Gold.

No Comments