This article was written by Wolf Richter and originally published at Wolf Street

There were some delicate morsels in the Fed’s monetary policy announcement today, none of them a surprise, but the nuances were perhaps such that some folks’ hopes got a little jostled, with the 10-year Treasury yield jumping 10 basis points in a matter of minutes and the Dow falling 265 points.

Projected rate hikes move closer.

The Fed’s projection per its “dot plot” pulled the first two interest-rate hikes into 2023, up from no rate hike in 2023. The “dot plot,” which represents the median of the FOMC members’ projections for future interest rate levels, is “to be taken with a big grain of salt,” Chair Powell said during the press conference.

This was perhaps a nod to the prior dot plot in March that had noted zero rate hikes in 2023 and now has already been obviated by events – these events being red-hot inflation. The dot plot is “not a great forecaster of rates,” he said.

Two upward “technical adjustments” to administrative interest rates.

The Fed’s monetary policy committee announced today that it raised two administrative interest rates “in order to keep the federal funds rate well within the target range and to support smooth functioning in money markets.”

It raised the interest it pays the banks on required and excess reserves, the IOER, to 0.15% (from 0.1%). And it raised the offering rate for overnight reverse repos (RRP) to 0.05% (from 0.0%).

I expected that the Fed would undertake these “technical adjustments,” as the Fed has been struggling mightily with its overnight reverse repo operations, now totaling over $500 billion, to drain the tsunami of cash sloshing through the banking system that is causing all kinds of issues.

The goal of those rate hikes is to put a floor under money market rates and to keep the federal funds rate in the middle of the Fed’s target range (0.0% – 0.25%). The Effective Federal Funds Rate has been at 0.06% recently, with a good portion of trades at or below 0.04%; the Fed would like it to be around 0.12%.

Inflation red-hotter than expected.

“If we saw signs that the path of inflation or longer-term inflation expectations were moving materially and persistently beyond levels consistent with our goal, we would be prepared to adjust the stance of monetary policy,” Powell said in the press conference.

“We would be prepared to adjust the stance of monetary policy” was maybe a nuance too much for some folks. So lets see just how far the Fed is behind the curve.

The Fed ratcheted up its inflation expectations as measured by core PCE to 3.0% for 2021, up from 2.2% at the March meeting. For 2022 and 2023, it projects core PCE inflation to decline back to 2.1% and 2.2% respectively, just above its target range, with everyone still believing that the current increases above 2% are “temporary” and will unwind.

The last actual core PCE inflation rate – this was for April – was already higher than all of these projected rates, at 3.1% year-over-year, with the three-month annualized core PCE inflation jumping by 4.9%. This is the Fed’s preferred measurement of inflation. Inflation as measured by CPI came in much hotter in May.

Here are a few nuggets of what Powell said about inflation at the press conference:

- “Inflation has increased notably in recent months.”

- “Inflation has come in above expectations over the past few months.”

- “The expectation is that high inflation readings will start to abate.”

- “We don’t in anyway dismiss the chance that it goes on longer than expected, and the risk could be that inflation expectations” rise above our goal. “When we see that, we would not hesitate to use our tools.”

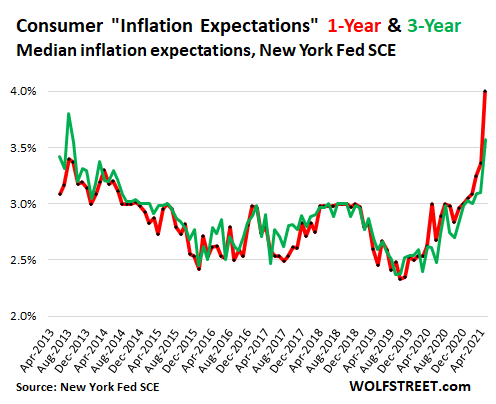

Alas, inflation expectations jumped to 4.0% for the 12-month outlook and to 3.6% for the three-year outlook, according to the New York Fed:

So the Fed should be getting nervous. And he said:

- “There is so much uncertainty,” and “we need to see how it develops over the coming months.”

- “Yes, there is a risk inflation will be higher than we thought. If we see inflation move above our goal persistently enough, we would be prepared to use our tools to deal with that.”

The Fed “had a discussion today” about tapering.

“The near-term discussion is the path of asset purchases,” not raising interest rates, Powell said, based on the doctrine that ending the asset purchases would precede rate hikes, same as last time. Here are some of Powell’s other nuggets on tapering:

- The Committee “had a discussion today” about tapering, and it will have discussions at “future meetings.”

- “We will provide advance notice” … “to give people a chance to adjust their expectation.”

- “Tapering will be “orderly, methodical, and transparent.”

The Fed is officially no longer talking about talking about tapering. It’s talking about how and when to taper.

All this boils down to this: The Fed is so far behind the curve, it’s no longer funny. But it is now trying to slow down the pace at which it is falling further behind.

EDITOR’S NOTE: The Fed knows it is incrementally destroying the US economy; this is the primary reason for its existence. The Fed is a suicide bomber driven by globalist ideology. What we don’t know is which method they plan to use – Will they continue hyperinflating the dollar through traditional means, or, will they use sudden rate hikes as they did during the Great Depression to create more chaos? It’s hard to say. Either way, the economy cannot survive another major shock to the system.

– Brandon Smith, Founder of Alt-Market

3 Comments

Apparently, the Fed’s now-expected tapering and raising of rates explains the huge drop in the price of precious metals, which were being held as a hedge against hyperinflation.

Brandon, thank you for publishing articles such as these from other sites. I have already read some of them on other sites but some I haven’t and your choice of articles gives me good information.